At a time when every financial decision counts, many small and medium-sized businesses (SMB) can at least take some comfort knowing that there is a wide variety of lending tools available if needed.

Today’s entrepreneurs can choose between credit cards that generate rewards; commercial loans; Bank loans; buy now, pay later (BNPL); lines of credit and much more.

But, according to “Lending dynamics for small and medium-sized businesses: trends, tools and decision factors”, a PYMNTS Intelligence and US Bank collaboration, SMEs need to consider a variety of factors before selecting the lending tools that make sense for them.

The size of a company, its revenue levels, leadership objectives, cash flows and expenses must be taken into consideration. SME executives should also consider how flexible and accessible they want their lending options to be.

Different priorities shape the final decision. For example, although 73% of all SMEs surveyed use revolving credit, low-income SMEs (those earning less than $1 million annually) use fewer lending tools, on average, than their high-income counterparts (those who earn US$10 million or more per year). ). In fact, low-revenue SMEs tend to prioritize immediate working capital needs and financial stability relatively more than high-revenue SMEs, which focus more on business expansion and growth objectives.

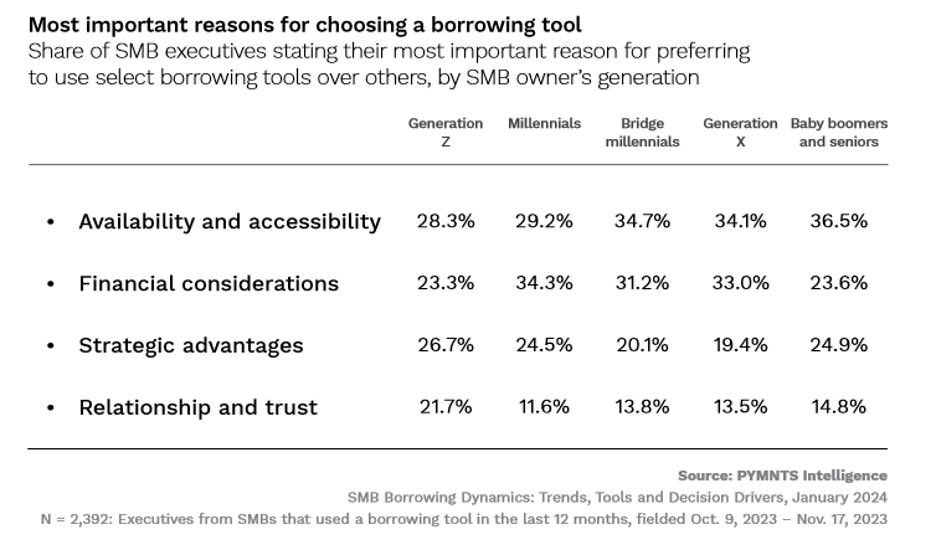

When evaluating and using lending tools, 75% of SMEs cite availability and accessibility of funds as a key concern, highlighting SMEs’ basic but essential need for flexible financing solutions. However, 71 percent point to financial considerations such as favorable payment terms (33%), lower borrowing costs (26%) and the potential to boost credit scores (23%). Relationship and trust factors are significantly less important, with just 14% of SMEs citing them as an important consideration.

SME preferences in selecting lending tools also appear to be shaped by generational perspectives.

For example, as the figure above shows, 37% of SMEs owned by baby boomers and seniors emphasize the importance of credit availability and affordability, while businesses owned by Gen Z and millennials are less influenced by these characteristics, at 28% and 29%. respectively.

Financial considerations, however, are more important for small and medium-sized businesses owned by millennials (34%), mid-millennials (31%), and Generation X (33%), compared to baby boomers and seniors (24%) or Generation Z (23%).

Interestingly, although only a few years separate millennials from Gen Z small and medium business owners, data shows that younger entrepreneurs tend to highly value relationships and trust in their financial institutions, with 22% saying these are the main factors – almost double the 12% share of the millennial generation. the Owners.

This data offers insights for lenders looking to work with small and medium-sized businesses. In other words, lenders must take into consideration what preferences appeal to the business owner before suggesting products.