Allegiant Travel Company Stock Is Not Impressive: Are There Advantages? (NASDAQ:ALG)

Angel Di Bilio/iStock Editorial via Getty Images

As of December 2023, Allegiant Travel Company (NASDAQ:ALG) opened its long-awaited Sunseeker Resort, diversifying Allegiant’s business, which prior to opening was primarily focused on passenger transportation and, to a lesser extent, resort-related revenue.

The Company released its first quarter results on May 7, 2024, providing some insights into performance and expectations for Sunseeker Resort. The results beat analyst estimates by $11.18 million in revenue and beat EPS estimates by $0.12. While the results beat analyst estimates, I found the earnings to be somewhat underwhelming. In this report, I discuss why I wasn’t very pleased with the results and update my price target for the stock.

Allegiant Travel Company Is Stuck in a Cost Trap

Loyal travel company

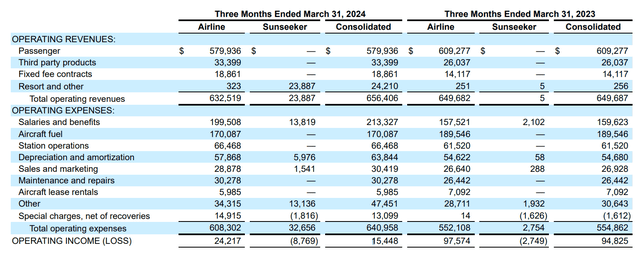

Total revenues increased 1%, while a $17.2 million decline in airline revenues was more than offset by Sunseeker’s revenue growth. The new resort, however, is off to a challenging start, as its opening in December was far from the ideal time to open. While Sunseeker Resort has potential for Allegiant Travel Company, there is obviously some learning curve involved in finding the right ways to market, price and promote. For the full year, the company now expects an EBITDA loss of $15 million for the resort.

The reason why the results didn’t impress me is mainly the performance in the airline segment. While revenues decreased by $17.2 million, we saw costs increase by $56.2 million despite a lower fuel bill. This was primarily driven by a $42 million increase in wages. Capacity increased by just 2%, so we see that modest increases in capacity are not allowing Allegiant Air to stabilize costs or revenue. Total passenger revenue per available seat mile decreased by 4.8%, while unit costs excluding fuel increased by 18.5%. So what we are seeing is that due to attrition, Allegiant Travel Company has not been able to increase its capacity and the company has now increased wages but is increasing the cost base more than Allegiant can apparently expand capacity without. compromising unit revenues and harvest.

What is Allegiant stock price prediction?

The Aerospace Forum

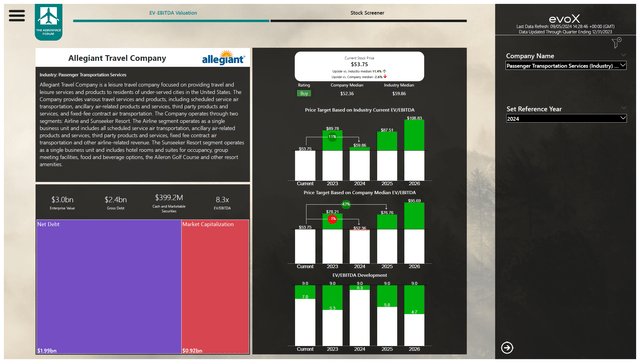

Much of the year will be focused on Allegiant reducing unit costs, which it hopes to achieve by the fourth quarter as modest growth in capacity adds up to an easier comparison. Sunseeker Resort will be in ramp-up mode this year, and I expect it will take until 2025-2026 before we see prices and occupancy at desired levels. Based on my expectations that Allegiant will continue to increase debt over the next several years to maintain a minimum of $400 million in cash and cash equivalents and a broader than normal time frame to evaluate its performance relative to benchmark, I’m rating the shares a buy. with a price target of $76.76 representing an upside of 43%. However, the risky nature of the investment opportunity must also be highlighted, given the cost challenges faced in passenger airline operations, as well as the learning curve and acceleration of Sunseeker Resort, making this a speculative purchase.

Conclusion: a challenging year for Allegiant Travel Company, but with prospects

I believe 2024 will be dedicated to controlling costs in the airline business and at the same time trying to increase results at Sunseeker Resort. Sunseeker Resort has a lot of potential, but it will take a while before full run rates are reached. Considering all the risks, I believe Allegiant Travel Company is a speculative buying opportunity with significant upside.

If you want full access to all our reports, data and investment ideas, join the Aerospace Forumthe #1 aerospace, defense and aviation investment research service on Seeking Alpha, with access to evoX Data Analytics, our in-house developed data analytics platform.